Venture Capital : re-model for growth

Venture Capital (VC) industry has been the corner stone of raising some serious seed capital funds for start-up entrepreneurs for many decades. Entrepreneurs typically infuse initial funds from their own pocket followed by friends & family and angle round, before raising funds from a VC firms.

VENTURE CAPITAL

Gaurav Sanan

5/10/20165 min read

Venture Capital (VC) industry has been the corner stone of raising some serious seed capital funds for start-up entrepreneurs for many decades. Entrepreneurs typically infuse initial funds from their own pocket followed by friends & family and angle round, before raising funds from a VC firms. One of the most prestigious tech name standing tall today is 'Amazon' that had raised $8Mn in 1995 from Kleiner Perkins Caufield & Byers (VC firm) generating 55,000%+ returns for the firm in 1999 (via Amazon's IPO).

Achilles heel for the VC industry has been it's inability to provide the desired returns to it's investors in the past and generally skewed cost structure favoring the management team over the investors. Let's first understand a typical Venture Capital returns framework under:

I. Understanding the VC firm setup:

Venture Capital Investment is a long term high risk investment that requires a lot of investor patience and faith in the model. Undoubtedly the risk and returns are supposed to be high given the riskier invested asset class (early to mid-life cycle start-ups) as otherwise the investors would be prudent enough to invest in Government Bonds or Bank Fixed Deposits or other stable assets.

A typical VC has founders & executive team (termed as “General Partners” or “GPs”) and external investors (termed as “Limited Partners” or “LPs”). The Venture Capital firm is setup by GPs as a legal entity that in-turn reaches out to various LPs for raising VC capital funds.

During the tenor of the VC fund (~10 years), GPs would focus on evaluating investment proposals from entrepreneurs and endeavor to make necessary investments thereby creating a diversified portfolio of investee companies.

Being a Venture Capitalist to me is like being more of a psychologist (Keith Rabois, Paypal, Linkedin, Slide and Square)

II: Returns Framework

LPs: They make around 2%-2.5% of the committed capital / fund value / invested capital during the tenor of the VC firm. Further they make additional 20% of the profits generated in excess of the capital commitment (termed as "Carried Interest").

GPs: They make around 99% of the return generated by the VC firm till such time their initial capital commitment is recouped. Post that, they garner the balance 80% of the excess returns generated over the capital invested.

III: Gauging Returns / Analysis

In order to understand the returns, there is no better way of looking at a sample VC firm size of say S$400Mn capital. Based on carefully chosen assumptions (stated below), the investor returns seem to reflect the below pattern:

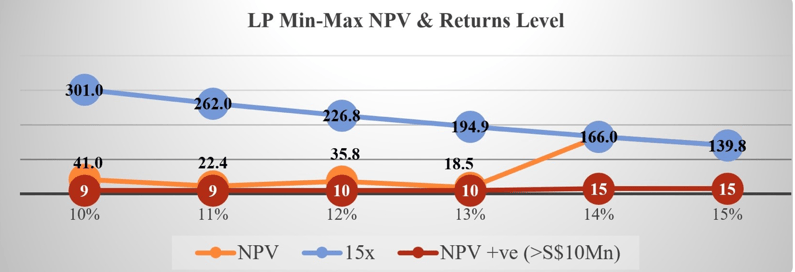

a. Return for LPs: Effectively a standard VC model mandates a minimum returns generation of min 9x / 10x times over the ~25% of the invested capital generating returns. This is the base minimum returns required for the LP investors to get back their initially invested capital along with a negligible return.

The horizontal base line % represents the discount factor or cost of capital (10%, 11%..15%), red line represents the base minimum returns multiple (7x, 8x and 9x) when the VC firm generates positive Net Present Value >S$10Mn, orange line represents the first positive NPV >S$10Mn at a particular discount rate and return multiple and the blue line represents the NPV at 15x returns multiple at any particular discount rate.

Basically at 10% discount rate above, if ~25% of the invested capital is productive, the LP would end up making between S$41Mn - S$300Mn if the return multiple ranges from 9x to 15x respectively.

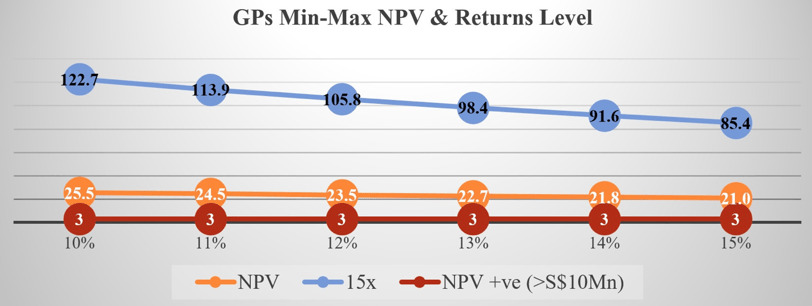

b. Return for GPs: Well, the GPs are the most interesting category of the investors to evaluate from the VC returns parlance. Even at 3x returns for the ~25% of invested capital generating returns, the GP can make returns in range of S$26Mn - S$123Mn, that's phenomenal.

The horizontal base line % represents the discount factor or cost of capital (10%, 11%..15%), red line represents the base minimum returns multiple (7x, 8x and 9x) when the VC firm generates positive Net Present Value >S$10Mn, orange line represents the first positive NPV >S$10Mn at a particular discount rate and return multiple and the blue line represents the NPV at 15x returns multiple at any particular discount rate.

Basically at 10% discount rate above, if ~25% of the invested capital is productive, the LP would end up making between S$41Mn - S$300Mn if the return multiple ranges from 9x to 15x respectively.

b. Return for GPs: Well, the GPs are the most interesting category of the investors to evaluate from the VC returns parlance. Even at 3x returns for the ~25% of invested capital generating returns, the GP can make returns in range of S$26Mn - S$123Mn, that's phenomenal.

Summary:

We can definitely see the skew in the returns generated by the VC firm for GPs under the current business model. Infact VC firms are seeing lot of disruption with respect to their business model on various fronts including returns.

We also need to take cognizance of the fact that there are competing fund raising platforms that now provide entrepreneurs with desired growth capital without diluting promoter shareholding (crowdfunding does not mandate shareholding dilution). Further as per recent reports, a long anticipated regulatory change [Title III of the Jobs Act] this month may allow retail investors (unaccredited investors) to join in start-up investor community on pari-passu terms hence opening up the possibility of platform based VC fund raising and distribution.

There is clearly a need for VC business re-modeling and a radical re-think on end-to-end model. Infact most of the investors prefer a niche agenda VC firm that can target companies with vertical specialization, focus on specific entrepreneurial demographics (take example of Jungle Ventures in Singapore that focuses on mid-career employee's instead of 20 something college drop-out / freshers) etc.

It is an interesting industry with potential to maximize the gains with investors and Venture partners. Let's see if there is any interesting business model brewing up that can come and completely turn the tables by creating a win-win partnership for Investors and Investee Companies.

Financial Times article stating that investors have pulled out USD 15Bn on account of high fee (similar to VC industry – management fee and 20% of excess returns) recently – dated 24th April, 2016

http://www.ft.com/cms/s/0/72b5a244-06fd-11e6-9b51-0fb5e65703ce.html#axzz46jzZr4Hi

Basic assumptions for the cash flow model construction:

% of invested capital that will generate returns : ~25% (weighted average of 10%, 20%, 30% and 40% scenerio's)

Return Multiple (x times): Given the uncertainty, assume return multiple on the % invested capital that will generate returns ('a' above) to be in range of 3x till 15x

Capital drawdown from GPs: In tranche's during the first 4 years

VC firm tenor: ~10 years (can be longer where the new fund is raised to pay-off / raise investment in the existing fund)

Discount factor - test various discount ranges > 10% - 15%

This postings on Linkedin are my own and don't necessarily represent my employers positions, strategies or opinions