Value Creation through Supply Chain Integration

Supply Chain remains an integral part of any business, driving growth through efficient end-to-end (e2e) management of the key business processes, ranging from procurement, production, inventory, transportation till final cash realization

SUPPLY CHAIN

Gaurav Sanan

9/18/20168 min read

Value Creation through Supply Chain Integration

Supply Chain remains an integral part of any business, driving growth through efficient end-to-end (e2e) management of the key business processes, ranging from procurement, production, inventory, transportation till final cash realization[1]. With simulation of the supply chain requirements, a business learns about in-depth demand patterns and its capabilities to remain ahead of the competitive curve.

An efficient Supply Chain Management (SCM) translates into lower Cost of Goods sold (COGS) and/or establishes a unique leadership position through an iterative process of continuous improvements, driving growth eventually. The case in point being companies like Zara, Dell, Uber, Walmart, McDonalds that have managed to create a whole new line of business through process improvements around existing supply chains.

On the other hand, SCM remains inherently unstable for most companies. Two imperative parameters that feeds supply chain stability and creates value are ‘process integration’ and ‘timely exchange of information’.

Many institutional platforms and technologies have improved the information flow between supply chain stakeholders using collaborative tools. However, there still exists a noted gap with geographical remoteness of global marketplace and “bullwhip” effect caused by demand & supply mismatch.

In view of the above, I have endeavored to evaluate an integrated working model for SCM convergence by looking at various process level innovations.

Physical and Financial Supply Chain overview

The concept of SCM has radically evolved over the last 4-5 decades. What started simply as inventory management and production planning process, evolved into Material Requirement Planning (MRP), Enterprise Risk Planning (ERP), Total Quality Management (TQM), Lean and later metamorphosed into integrated Supply Chain. The “manufacturer” is referred to as “Anchor” in this article, one who acts as Buyer (for its suppliers) and Seller (for its distributors / retailers). For the sake of understanding, the SCM concept can be broken into various sub-categories but let’s broadly categorize them into two main sub-categories:

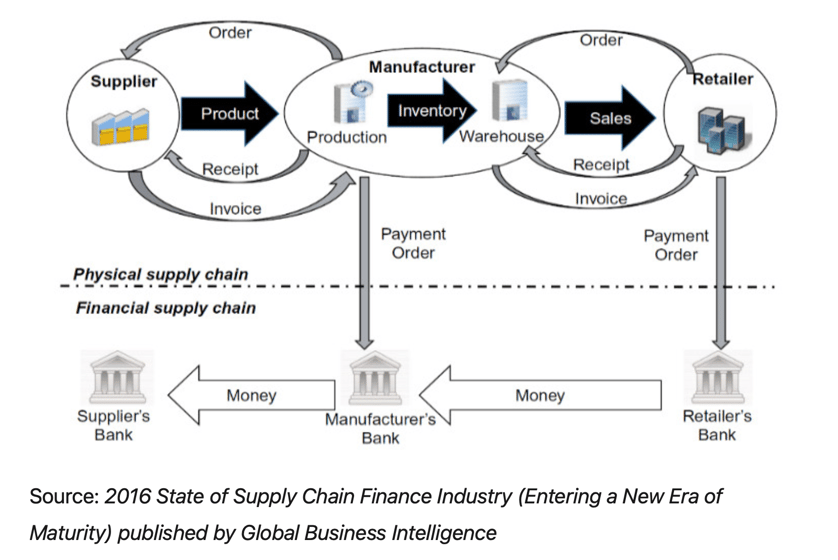

a. Physical Supply Chain (PSC) covers the entire chain from the supplier of goods/raw materials to the end customer, with its inter-related network of partners, contract manufacturers, suppliers, packers, logistic players, re-sellers working together within the defined parameters. The goods move from supplier to the Anchor Buyer (main manufacturer) passing through the procurement, production, logistics and warehousing steps. Finally, the goods are sold to the end customer/ buyer by the retailer

b. Financial Supply Chain (FSC) involves movement of funds and interjects with Physical Supply Chain in order to create liquidity through various Supplier or Buyer led solutions; with or without an enabling technology. The finance is provided by banks and is repaid from the collection[2] received from end customers that passes back through the entire supply chain. Refer the picture to see the movement of goods (PSC) and funds (FSC) across the entire supply chain.

It is pertinent to note that there are various handover nodes (point of intersection of PSC and FSC) wherein some redundancies creep into the SCM network. These nodes where the handover is delayed or not linear leads to creation of bottlenecks in efficient movement of information between the supply chain stakeholders.

In order to explain the above point, we can better understand it through the need of documentation required to seek services such as logistics and financing of the same cargo (illustration). The logistics provider and financing banks generally need similar set of information in order to undertake shipment and funding respectively. However, logistics companies and banks duplicate information at their end. Further the buck does not stop there, they spend a lot of time trying to reconcile Purchase Order (PO) with Invoices and Invoices with Bill of Lading (transport document).

Broad overview of Supply Chain Strategies

A holistic view of the supply chain not only provides visibility to the inventory (movement and consumption of inventory) but also enables superior information flow between transacting parties. Anchor needs to focus on one or more of the SCM strategies viz Differentiation (process/product e.g. Dell), Cost Advantage(Cost leadership e.g. McDonalds, Walmart), Resilience through creation of a sticky eco-system (e.g. Apple) and Dynamism through extremely entrenched integration (e.g. Zara). It uses a blend of economic / competitive drivers complemented with listed enablers (communication, relationship management etc) to improve overall business performance.

End-to-End view of FSC

The basic grain of FSC hinges on driving comfort on the Anchor’s balance sheet and its credit rating. The lenders try to arbitrage the credit standing of an Anchor to provide cost effective funds to its suppliers and/or distributors. Any lender generally tries to establish buying linkages of Anchor with its “Suppliers” & selling linkages with its “Distributors”.

The Anchor-Supplier or Anchor-Distributor linkages are tested through simple yet powerful measures like relationship vintage, transacting history, sales & payment track record, goods/services reject ratio, days past due history etc. These measures help in establishing the criticality of the supplier / distributor to the Anchor. The criticality determines the quantum of funding ultimately made available to supplier / distributor.

Further, from the risk mitigation viewpoint, the finance provided to suppliers is multi-staged to keep the risks under control. Stage wise supplier financing helps the lenders to remain closer to the PSC on account of intersecting nodes between PSC and FSC and gradual shift of risk from Supplier to Anchor. On the distributor side, most of the Anchor’s want the distributor risk to be borne by the bank’s and prefer to receive cash payment upfront for goods / services provided by them to the distributors. In some cases, they extend financing to some select distributors to keep the supply chain sticky or based on competitive pressure.

Linking PSC and FSC together

Anchor level closed loop integration of various internal departments needs to be achieved beforehand an organization thinks of inviting external stakeholders. Post successful internal integration, the key to well entrenched supply chain is seamless integration with its supplier’s, distributor’s and customer’s. The external integration is quite difficult to attain however few companies like “Li and Fung” have proven success in this domain by making their manager’s work in supplier’s factory floors. IKEA is another classic example that embodies the internal and external integration quite well. IKEA has achieved this by sharing strategic plans & information with suppliers in a timely manner and keeping them closely knit. Value Creation for an organization is only possible when PSC and FSC are interlinked seamlessly across the process.

Possible Approaches for Integrated SCM

Alibaba has managed to create a supplier marketplace financing opportunity by closely tracking the sales and customer feedback of their vendors. Taking a cue from this, I have listed some of the key process centric innovations that can drive creation of an integrated SCM platform:

a. Creation of Devolved, collaborative, supply chain clusters

It is widely accepted that with the increase in number of supply chain nodes the probability of stable operations goes down. However, a wide scale supply chain integration is only possible if we endeavor to create smaller collaborative clusters co-existing within the preamble of a lager all-encompassing SCM. In particular, Auto industry shows this devolved cluster centric approach for their parts suppliers. For e.g. supply chain platform focusing only on Battery and Plastic molding cluster, Electrical components cluster, Gear box cluster needs to be on-boarded first and later integrated with each other.

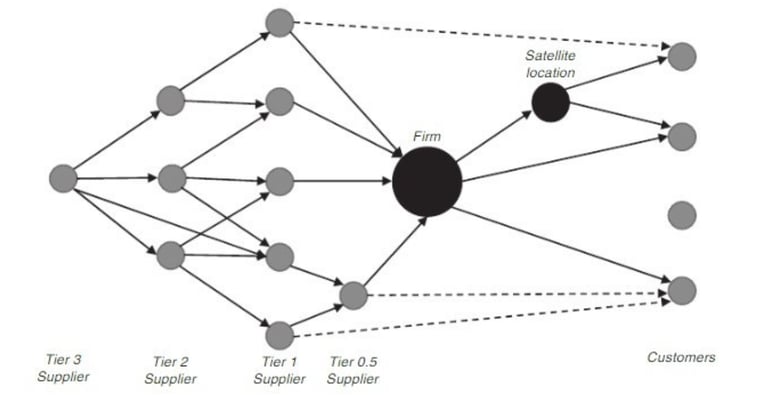

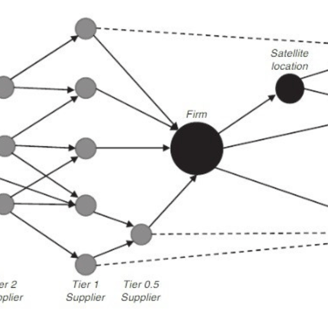

b. Integrating second and third tier supplier’s and widening the supply chain network

From a basic understanding of integration, we need not stop at the last mile (or Tier 1 or Tier 0.5 refer the screenshot on right) suppliers to the Anchor. In fact we need to bring in the Tier 2 and Tier 3 suppliers onto the Integrated SCM platform.

If we are able to achieve this through the platform approach, the Anchor will be able to direct sourcing of raw material from specific Tier 2/3 suppliers ensuring consistency in sourcing and end-to-end integration. For e.g. in case of Clothing Retailer., the Anchor can mandate Tier 1 / 0.5 suppliers to source “Buttons” or “Zippers” for garment from specific Tier 2/3 suppliers.

From the FSC perspective, the portion of funds that was initially supposed to be extended to Tier 1 suppliers will now get channelized to Tier 2 and Tier 3 suppliers for sourcing raw material for Tier 1 and 0.5. This is a value accretive process to the Tier 2/3 suppliers, provides better understanding to the lenders, integrate end-to-end stakeholders for Anchors and provide a holistic view to better deliver on Supply Chain strategies (Cost Advantage, Differentiation, Resilience, Dynamism).

c. Vertical focus SCM platform

The key idea here is to look at some sticky supply chain ecosystems e.g. Automobile, Global Retailers, Tech companies and evaluate the supplier stickiness to build niche fund-able asset class in this segment. Most of the existing banks and crowd-sourced platforms have a general vertical agnostic approach where they look at any investment grade Anchor’s accepted invoice for financing. This vertical focused approach will help the entire eco-system and attract investors with better risk understanding of a specific sector.

d. Pre-shipment financing for suppliers

There is definitely value in looking at early stage financing for the supplier. Most of the institutions may look at specific Supplier-Anchor relationship and manually credit underwrite supplier risk. Such institutions look for collateral to extend such funds to supplier and hence de-merits the value of SCM based transactional financing.

e. Early Process Engagement

Early engagement with the procurement team of large Anchor’s is quite an important and effective strategy. We need to start with supply chain solutions from purchase/procurement manager’s perspective and the approach of looking it from Treasury / Finance angle as a starting point needs to change.

f. Cash Conversion Cycle (CCC) track

Efficient supply chain integration places all essential resources of partners together and connects all functional processes in order to effectively use available resources. Linking of FSC with PSC enables an efficient track of CCC / C2C thereby providing better visibility of movement of funds along the supply chain. This liberates the funding gaps across many supplier / distributors and ultimately frees-up the tied up working capital of Anchor.

g. Inviting more players (like logistics, warehouses) to the club

The distributed ledger technology can be put to efficient use by banks, logistics partners, warehouses to empower the interested stakeholders to look at real-time status of any particular transaction. This also prevents double financing and minimizes the chances of any fraud. This needs a wider industry cross collaboration to bring this into wide spread acceptance and usage.

Platform approach

In nutshell, the above ideas can help in synthesizing some value capture opportunities that exist today. By applying the process lens, a niche vertical specific supply chain platform can be enabled that will provide end-to-end integration along with various logistics providers, warehousing companies, supplier and distributors. It entails bringing together many investor classes including Qualifying retail investors, Insurance companies, Fund houses, Banks and Non-Banking Finance companies onto such platform to create cost competitive liquidity[3] for the eco-system. Such platforms work well when they are integrated with Anchor’s ERP, Electronic payment system and bring in procurement as well as treasury teams of Supplier-Anchor-Distributor together.

This posting on Linkedin is my own and don't necessarily represent my employers positions, strategies or opinions

[1]Cash Conversion Cycle (CCC) or Cash-to-Cash (C2C) cycle measures “the average days required to turn a dollar invested in raw material into a dollar collected from the customer”

[2]The timing of funds collection and eventual payment may differ as manufacturer may need to pay supplier upfront or supplier may have to finance the payable cycle depending on his bargaining power.

[3]Given the zero to negative interest rate environment and supressed yield in other asset classes, many corporates are actually quite willing to use their own balance sheet (excess cash on their balance sheet) to extend financing to their supplier’s / distributors using Dynamic Discounting (transaction based negotiated discount) approach.

The intent is to keep is simple, relevant and workable to meet the end needs.

This post first appeard on Linkedin (here) is my own and don’t necessarily represent my employers positions, strategies or opinions

Get in touch