A case for Medium Enterprises

Small & Medium enterprises (SMEs) remain an important and integral development foundation for most of the emerging economies. They have the ability to transform the wealth of nations and approx 70% of them operate in the emerging economies as per the World Bank survey of 132 economies.

SUPPLY CHAINPRIVATE CREDITTECHNOLOGY

Gaurav Sanan

1/5/20164 min read

Why Medium Enterprises Matters

Well, Small & Medium enterprises (SMEs) remain an important and integral development foundation for most of the emerging economies. They have the ability to transform the wealth of nations and approx 70% of them operate in the emerging economies as per the World Bank survey of 132 economies.

The maximum density of SMEs is in the regions such as Indonesia & Brunei apart from dense presence of such enterprises in Central, Eastern & Southern Asia. It is the power of the distributed ownership and sheer volume that makes this whole segment attractive for the entire ecosystem. Given the focus on high end manufacturing and outsourcing, these enterprise are rightly termed as backbone of the nation.

Apart from the economic view point, this segment also provides large scale employment opportunities and feed into large corporate & public companies thereby bringing in innovation and outsourced process efficiencies at the local level.

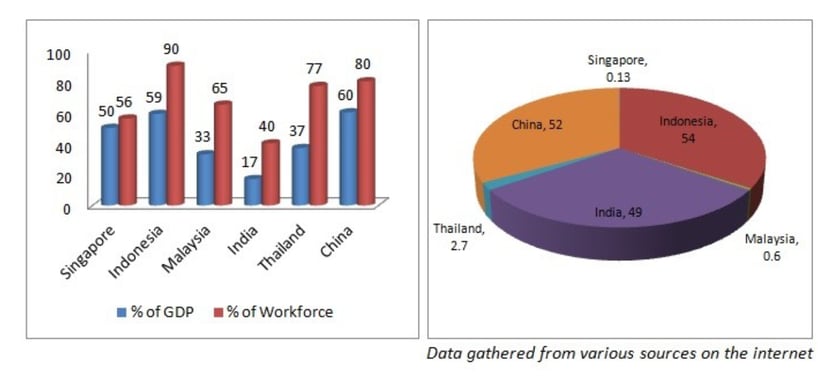

Broad level view of the key numbers for SME segment is as under:

(# of SMEs per 1000 people)

olume of SMEs operating in South and South East Asia is provided above in the map (right hand) with China, India and Indonesia leading the frontier.

While there is definitely value at the bottom of the pyramid and it appears that most of the effort is expended thinking of “Small” enterprises and building scale for them, it leaves a conceivable gap in terms of meeting the needs of Medium Enterprises. Most of the large corporate entities (private and public) and MNC enterprises have integrated with Mid-Market enterprises to help them in their supply / distribution chain. Mid-market enterprises bring in a lot of stability to the whole setup.

May be it’s a right approach to first re-look at the definition of Medium Enterprises as different countries deploy divergent methods in trying to contextualize this segment. Most of the countries define SMEs by using combination of employee strengthen, turnover and / or investment in Plant & Machinery. For the sake of clarity, let’s assume that Medium Enterprises are the companies registering revenues in excess of $75Mn/$100Mn upto $250Mn threshold on an annualized basis. These companies are not large or established corporate’s yet, but they are also not Small Enterprises either and hence a strategically important segment to grow. Middle Enterprises signify those enterprises that have managed to grow in spite of all the challenges and decoded the formula to grow in an extremely competitive environment.

Now let’s address the moot question, why should we lay importance on the needs of this particular sector over the volume and mass of sub $75Mn Small Enterprises and the credit worthiness of large corporates. One true testament of these enterprises is the resilient character as they have not only survived but also grown in spite of the many hurdles (viz insufficient capital, micro management and rigid policies) to break into the mid-club.

The previous statement also comes with a pinch of salt as these companies are still promoter / family driven and carry more credit risk in terms of quantum (more credit appetite in comparison to small enterprises) and relative comparison with large enterprises.

A typical characteristic of the companies operating in this segment reflect double digit growth and need for more capital / debt. One basic reason to focus on these enterprises is the “value potential” they offer on account of their growth agenda and needs. The quantum of funds required (equity / debt) and the returns offered make this segment attractive to both lenders / investors seeking higher returns.

Apart from financial numbers, the financial community likes the personal connect with the promoter’s / family members in this segment that mirrors the growth trajectory of these companies. Most of these promoters are not looking only for low cost funding but actually a genuine advice ranging from various business issues. Further these family members / promoters are valuable source of private banking / wealth management client base of the banks ultimately leading to more dollar value from the customer relationship standpoint.

Overall, these entities are systematically important for the general growth of the economy and impart the needed competitive to any particular industry. It may be prudent to assume that these companies contribute approx 20%-40% of GDP of major economies. During a recessionary time period, these companies definitely come under pressure on account of stretched accounts receivables from large corporates and delayed supplies from SME segment and hence needs to be watched more closely to build a robust portfolio. However, an adequate amount of debt and right amount of equity support can propel these companies into the large corporate league.

As I heard some of the promoters complain aptly, overfinancing is definitely bad but “under-financing” is a recipe for disaster. Maybe it’s time to look at these companies with a new broad lens and provide them with ample growth capital (the way capital is being poured to finance new venture’s / start-ups at the moment) looking for a more stable unicorn to generate profits for a longer period of time.

This post first appeared on Linkedin (here) are my own and don't necessarily represent my employers positions, strategies or opinions

Get in touch